Optimization

Stop guessing your portfolio allocation.

Set a goal, add your constraints, and let the optimizer solve for the allocation. Every result comes auto-backtested so you can see it actually held up.

How it works

From assets to optimal weights.

Choose your assets, set constraints, and pick an objective. The optimizer solves for the best allocation and backtests it for you.

Add assets & set constraints

Pick your universe and set per-asset and group limits. No shorting unless you allow it.

Choose an objective

Maximize Sharpe, minimize volatility or CVaR, target risk parity - eight objectives in all.

Get optimal weights

Receive the optimal allocation, automatically backtested so you can confirm it held up.

Objectives

Optimize for what you care about. Beyond mean-variance.

Eight objective functions, from classic risk-adjusted return to hierarchical risk parity - so the allocation matches your actual goal, not just the textbook one.

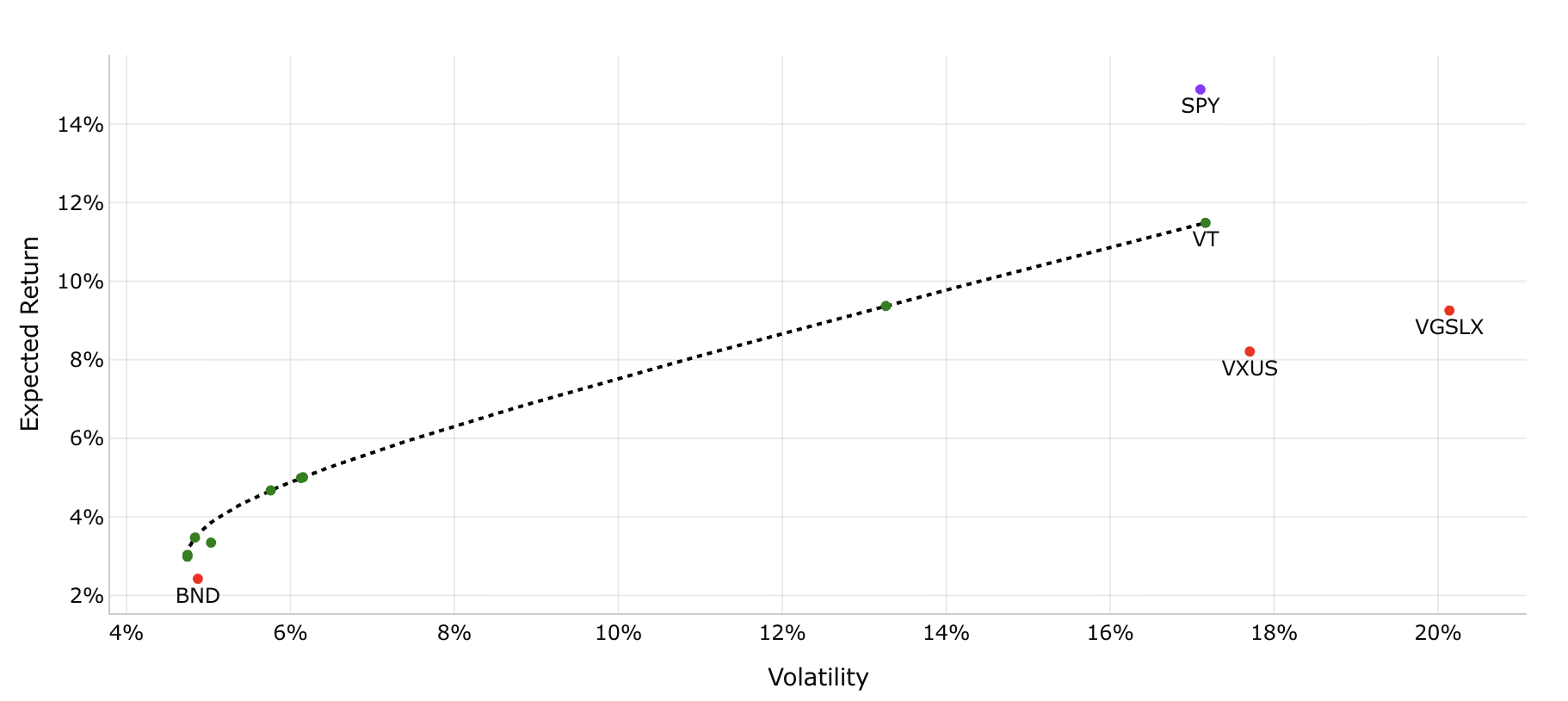

Efficient frontier

See every optimal trade-off.

Plot the full efficient frontier and use transition maps to watch how the optimal mix shifts across periods - so you can judge stability, not just a single point.

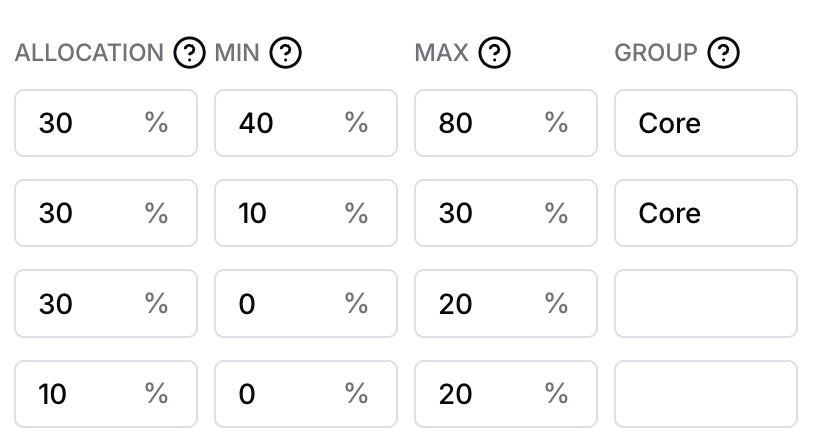

Constraints

Keep allocations realistic.

Set per-asset minimums and maximums, group constraints like 60% equities and 40% bonds, and a no-short toggle - so the result fits how you actually invest.

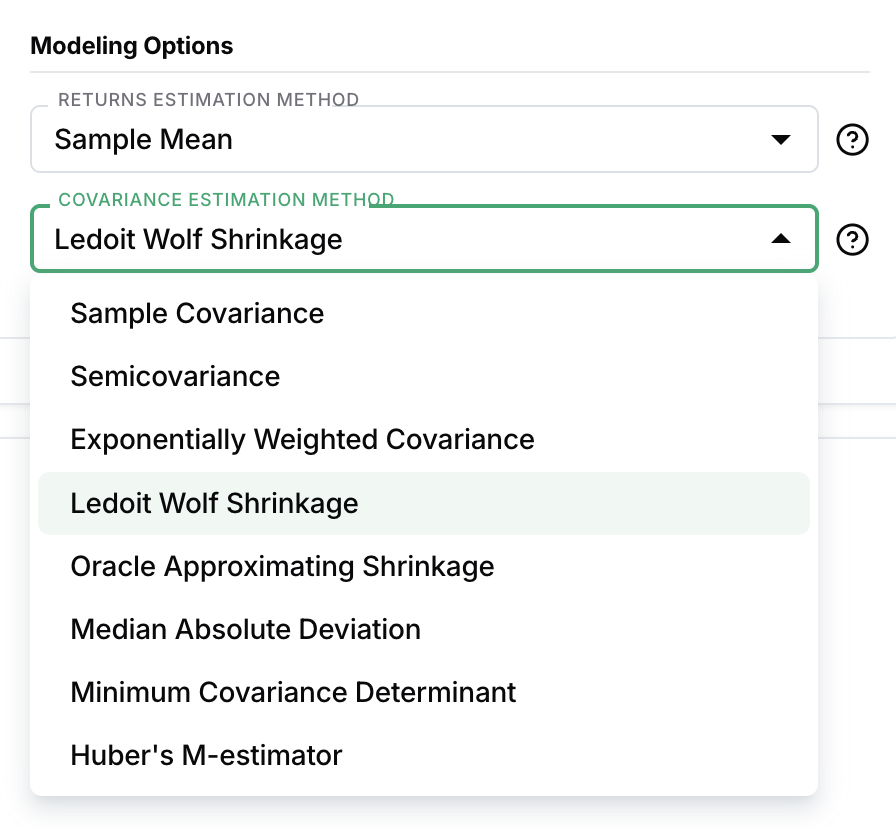

Estimation methods

Stable inputs, trustworthy weights.

Covariance shrinkage (Ledoit-Wolf, OAS), robust and CAPM-implied returns, or your own expected returns and volatility - because optimization is only as good as its inputs.

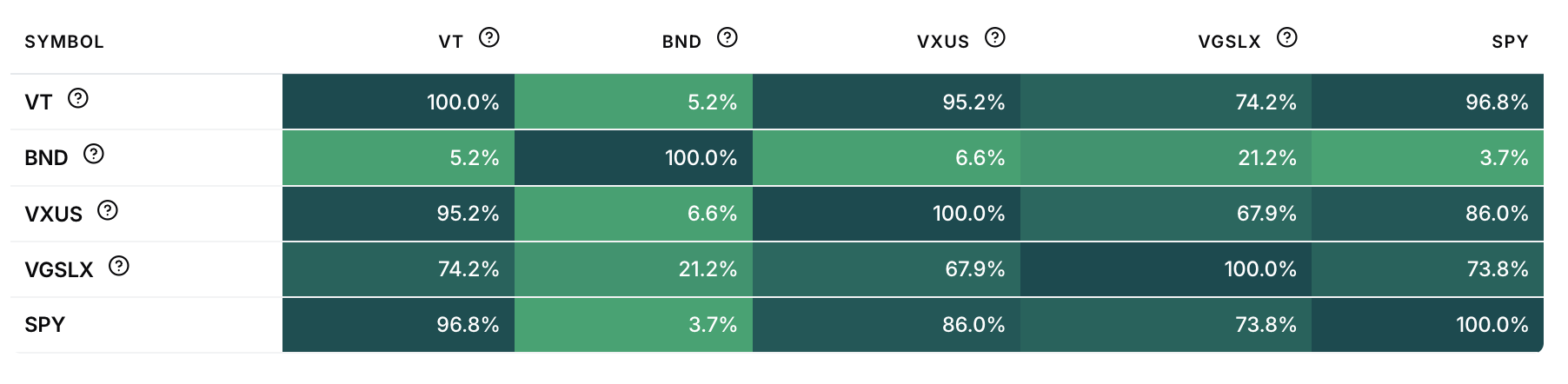

Correlation

See the diversification story.

Visualize the correlation and covariance matrix across your assets - so you understand the relationships the optimizer is working with and can judge whether the diversification is real.

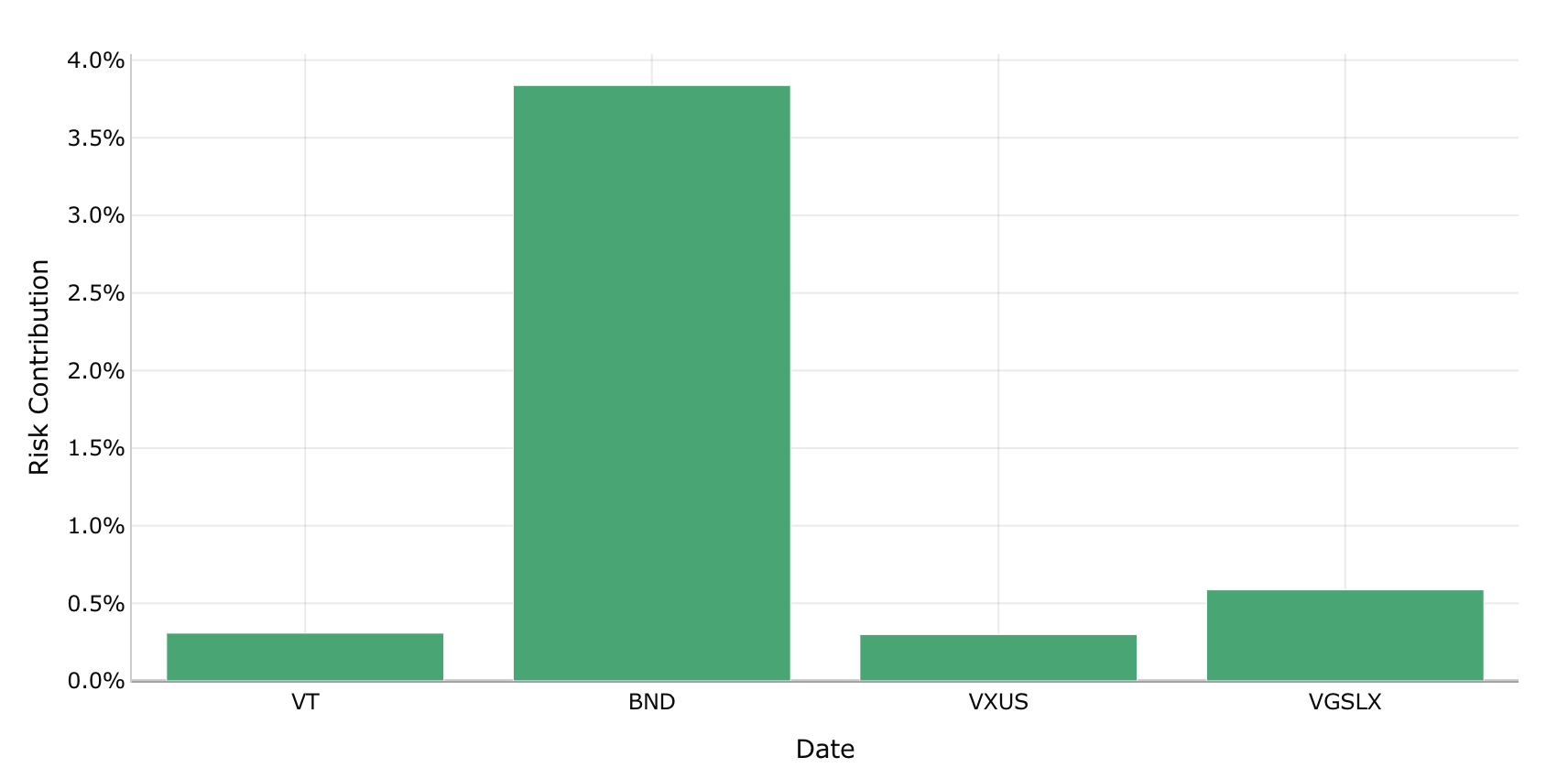

Risk Parity

Balance risk, not just capital.

Hierarchical Risk Parity (HRP) allocates so each asset contributes equally to portfolio risk - not equally by value. The result holds up better in volatile markets and requires no expected-return assumptions.

Capabilities

Everything in the optimizer.

Per-asset leverage

Custom Risk-Return Assumptions

Advanced Risk-Return Estimation

Allocation Constraints

Save & Share Reports

PDF & CSV export

40+ years of data

Stocks, ETFs, funds, crypto & bonds

Multi-currency

Correlation & covariance matrix

Find your allocation.

Set an objective, add constraints, and get optimal weights - backtested.

Optimize a portfolio